After three flat-to-down years, 2025 was the year venture funding came roaring back, and the numbers are genuinely staggering. Investors deployed $425 billion into more than 24,000 companies, up 30% year over year, in the third-highest venture year ever recorded. It included the largest private funding round in history at $40 billion. If you read those headlines as a founder, you felt one of two things: that capital was healthy and available again, or that everyone else was raising while you weren't. Both reactions lead you astray, because both assume the headline describes the market you operate in.

Half of every venture dollar went to one sector

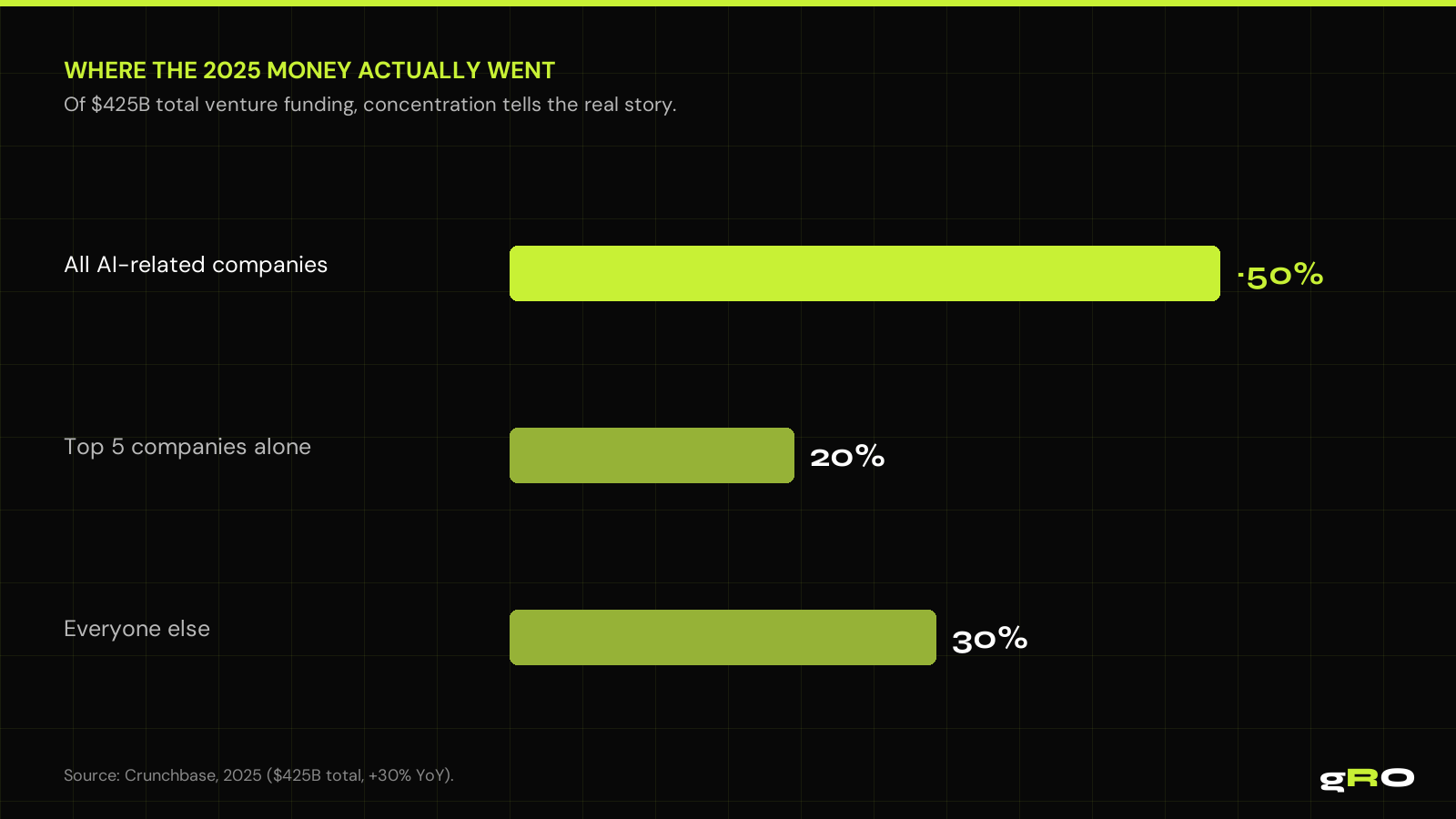

Strip the total apart and a very different picture emerges. Roughly 50% of all global venture funding in 2025 went to AI-related companies. AI funding alone hit $211 billion, up 85% year over year, surpassing even the 2021 peak. The top five companies raised $84 billion between them, 20% of all venture funding in a single year.

The private-market value concentrated into a handful of giants: SpaceX at an $800B valuation, OpenAI at $500B, Anthropic at $183B. The US share of global funding jumped to 64%, from 56% a year earlier. This is not a market that's broadly generous with capital. It's a market that made an enormous, concentrated bet on frontier AI and a short list of category leaders. The rising tide lifted a few yachts very high and left the headline looking like a flood.

Most companies your size raised under $5M

For the vast majority of SaaS companies (between $1M and $10M ARR, not building a foundation model), none of this describes the air they breathe. The Mercury data on actual early-stage companies makes the gap concrete: 73% raised under $5M in their last round, 22% under $1M, with a median seed around $2.5M. More than half hadn't raised institutional VC at all.

That's the real distribution: a record-breaking top, and a long body of lean, lightly-capitalized companies for whom \"the funding environment\" is a headline about other people.

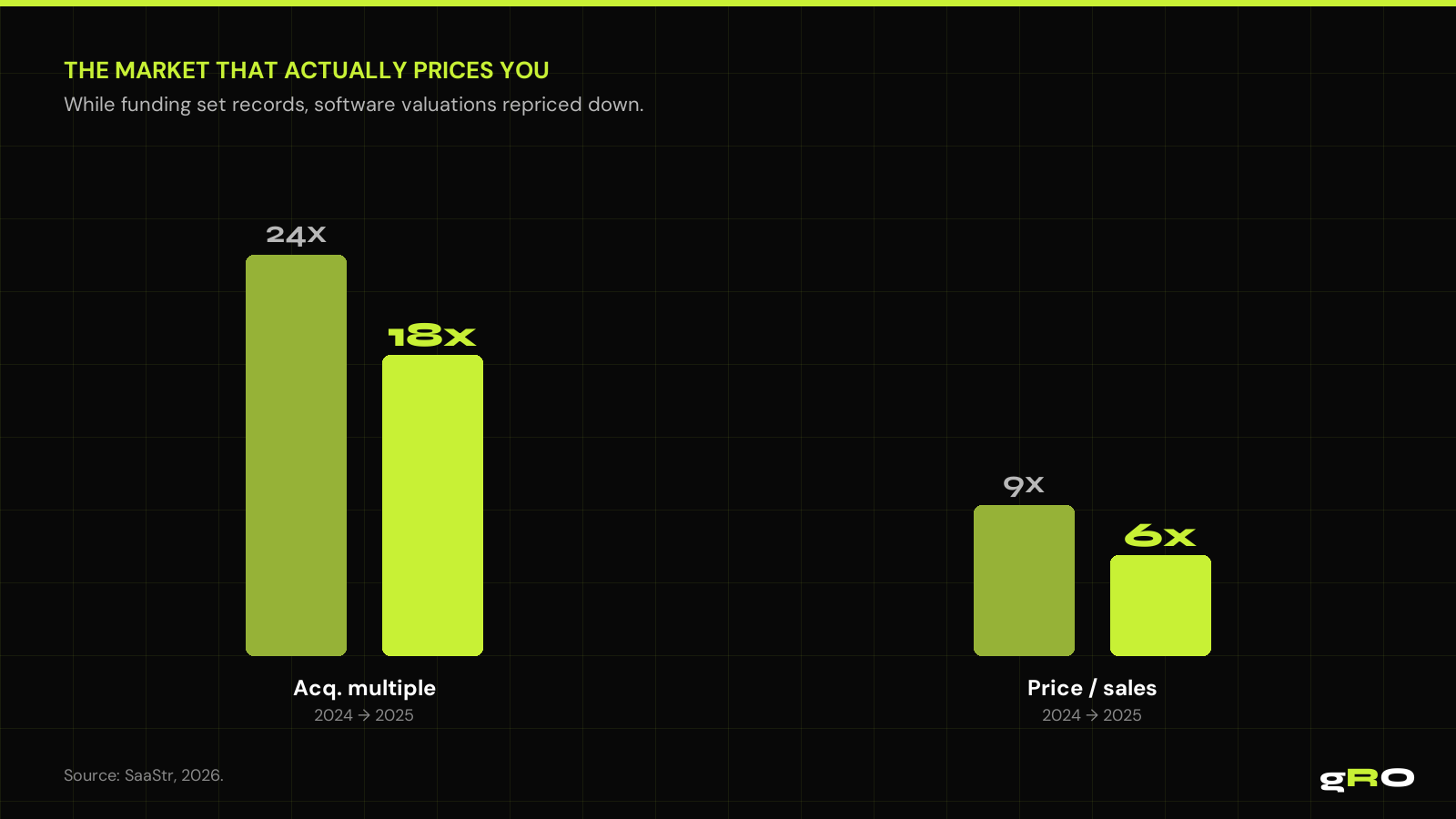

While funding set records, software repriced down

Here's where the disconnect turns costly. While the funding headline was setting records, the operating market for software was doing the opposite, repricing hard. SaaS acquisition multiples fell from 24x to 18x in a single year. Software price/sales ratios compressed from 9x to 6x, the lowest since the mid-2010s. The software index dropped 23%+, erasing $285B of market cap in a single day.

This is the market a normal SaaS company answers to: not the $40B AI round, but the multiple a real acquirer or investor will pay for real revenue. And that multiple got cut by a quarter in a year. Growth-at-all-costs, the strategy the 2021 peak rewarded, is being actively punished in the market that prices everyone outside the AI top tier.

The trap, in three steps

- You read the aggregate ($425B, biggest round ever) and absorb a feeling of abundance.

- You benchmark yourself against it: spend like capital is cheap, hire like the next round is a formality, optimize growth rate over efficiency.

- You get priced by the other market, where multiples fell 24x→18x and the question is efficiency, not speed.

Build for the market you're actually in

This is the climate Operator-Led Growth was built for. One senior operator owns the entire growth function (positioning, paid acquisition, lifecycle email, copy, analytics, forecasting, weekly optimization) with an AI agent fleet absorbing the execution volume. The model is, structurally, an efficiency bet: maximum owned-output per dollar, no coordination tax, no headcount built ahead of proof.

It matches the lean-by-default reality the data describes, optimizes for the metric the post-correction market actually prices, and keeps your operating tempo set by your funnel math, not by a headline about a $40B round you're not in. If a record-year headline is tempting you toward a spend-and-hire posture, run the other number first: what does it take to grow efficiently in a market that just cut software multiples by a quarter?

Sources cited in this analysis

- Crunchbase, Global Venture Funding In 2025 Surged As Startup Deals And Valuations Set All-Time Records

- Crunchbase, North American Startup Funding Soared 46% In 2025, Driven By AI Boom

- SaaStr, SaaS Markets Have Crashed in 2026 (multiple compression)

- Mercury, The New Economics of Starting Up 2025 (raise distribution)