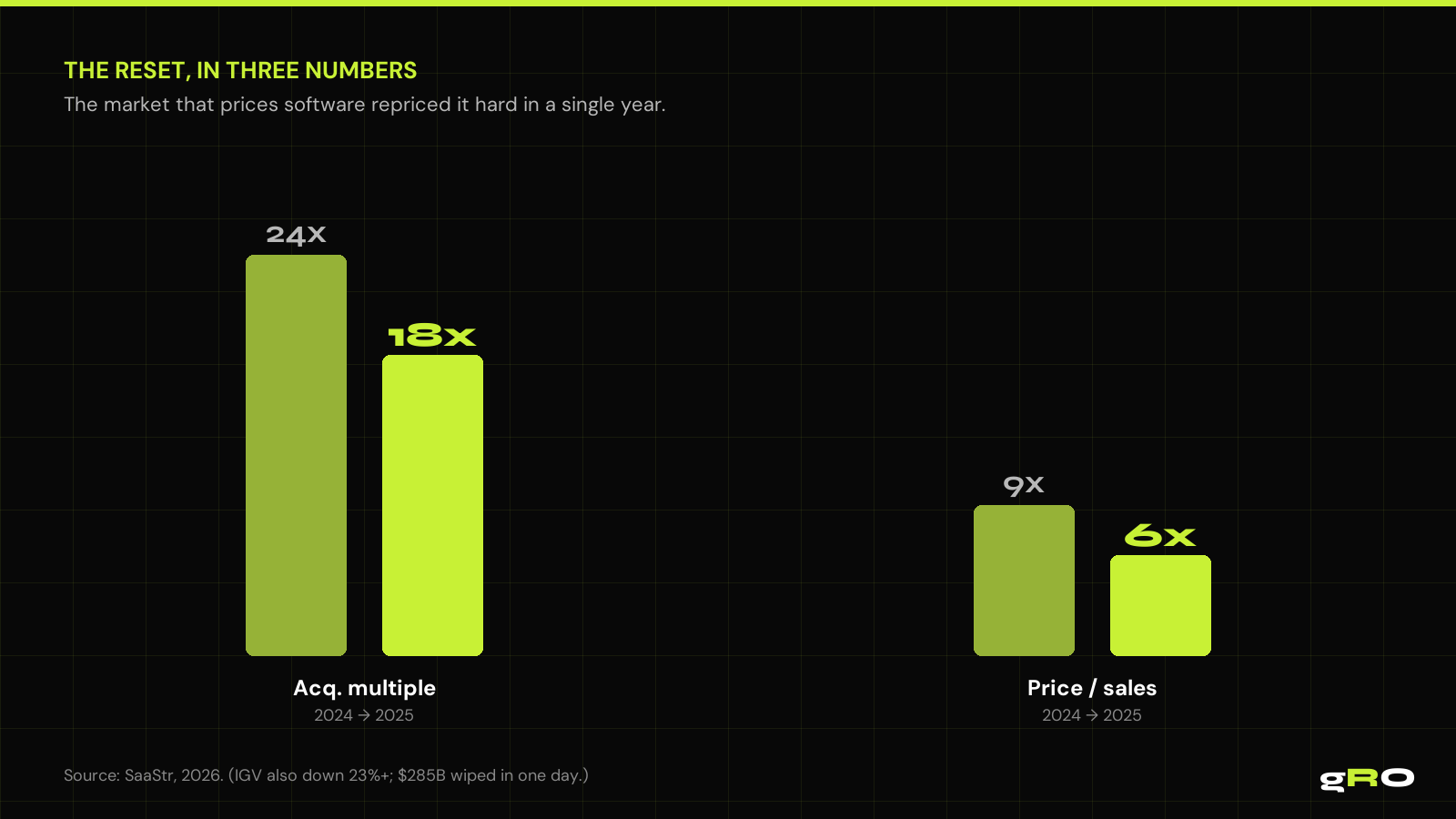

Through 2025 and into 2026, the market that prices software repriced it hard — and fast. SaaS acquisition multiples fell from 24x to 18x. Software price/sales ratios compressed from 9x to 6x, the lowest since the mid-2010s. The software index dropped 23%+, erasing $285B of market cap in a single day. The individual stories make it visceral: Figma traded down more than 80% from its high while growing revenue 40% year over year. That single data point is the whole article — the market stopped paying for growth alone.

The new multiple is the baseline

It's tempting to read a down year as a cycle that will revert. The structure says otherwise. From 2015 to 2025, more than 1,900 software companies were taken private by private equity in deals worth $440B+, all underwritten on the same thesis: sticky recurring revenue, high margins, predictable cash flow. Software became the collateral base for an entire private-credit market.

When multiples compress from 24x to 18x and P/S from 9x to 6x, the valuations those 2021–2022-vintage deals were underwritten at don't just wobble — many have been cut in half, and the debt behind them has to be repriced too. This isn't sentiment swinging back next quarter. It's the unwinding of a decade-long re-rating of what recurring revenue is worth. Plan as if 18x and 6x are the world, not 24x and 9x.

Growth-at-all-costs was rational — at 9x sales

For most of the 2010s and through 2021, growth-at-all-costs was a rational response to the prices on offer. At 9x sales and 24x acquisition multiples, a marginal dollar of revenue was worth so much in valuation terms that spending aggressively to capture it — even inefficiently — penciled out. Burn was a feature. The market paid for the top-line number and forgave the cost of producing it.

The reset removes the forgiveness. At 6x sales, the same marginal revenue is worth a third less, and the market now looks through the growth rate to the efficiency underneath — payback period, burn multiple, output per dollar. The Figma example proves it: 40% revenue growth, and the market still cut the price 80%. Founders running the 2021 motion in the 2026 market are optimizing for a buyer who left.

Applied to your next dollar

The reset lands on a lean operating reality. The Mercury data shows the modal early-stage company is already lean — 73% raised under $5M in their last round, 22% under $1M. So most $1M–$10M ARR founders aren't sitting on a war chest to spend through a repricing. They're allocating a scarce dollar in a market that now grades the allocation.

That turns every spending decision into the same question: does this dollar return efficiently, or does it just buy growth? A paid channel that \"works\" at a payback the old market forgave may not clear the new bar. A growth hire that adds capacity but not provable efficiency is a worse bet at 6x than at 9x. The reset doesn't say stop spending. It says every dollar is now graded on return, not just growth — so know which of yours clear the bar.

Where the marginal dollar compounds

- Fix the leaks before adding volume. Recovering efficiency from an existing funnel returns more than buying more traffic into a leaky one.

- Concentrate, don't spread. One channel owned to efficiency beats three at mediocre payback.

- Buy output, not headcount. Adding fixed salary to produce growth is the least efficient form of the marginal dollar.

- Measure what the market now measures. Payback period, efficiency ratios, revenue per dollar deployed.

An efficiency allocation of the growth dollar

Operator-Led Growth is, at its core, an efficiency allocation of the growth dollar — which is exactly what the reset rewards. One senior operator owns the full function with an AI agent fleet absorbing execution volume. No coordination tax, no headcount ahead of proof, every dollar pointed at provable return.

It optimizes for the metric the post-reset market actually prices, matches the lean capital reality the data describes, and puts the marginal dollar through the compounding order by design: diagnose and fix the funnel first, concentrate the channel, buy output instead of headcount. If you're not sure which of your dollars clear the new efficiency bar, that's the first thing to find out.

Sources cited in this analysis

- SaaStr — SaaS Markets Have Crashed in 2026. But Is Private Credit the Even Bigger Risk?

- Mercury — The New Economics of Starting Up 2025 (lean raise distribution)

- Equidam — Startup Valuation Delta H1 2025; KPMG — Startup Valuation (corroborating multiple compression)